Access proven resources for business success!

Discover how hibretOne can transform your ideas into reality.

Levelling-up for overlooked communities

The global Rotating Savings & Credit Association (ROSCA) market is worth $790billion. Help-To-Invest we hope will allow us to tap into this levelling-up opportunity.

A rotating savings and credit association (ROSCA) is an informal financial institution consisting of a group of individuals who make set contributions and withdrawals to and from a common fund. A ROSCA uses a common fund to which individuals contribute a set amount on a regular basis (usually monthly),

The global Rotating Savings & Credit Association (ROSCA) market is worth $790billion. Help-To-Invest we hope will allow us to tap into this levelling-up opportunity.

A rotating savings and credit association (ROSCA) is an informal financial institution consisting of a group of individuals who make set

The global Rotating Savings & Credit Association (ROSCA) market is worth $790billion. Help-To-Invest we hope will allow us to tap into this levelling-up opportunity.

A rotating savings and credit association (ROSCA) is an informal financial institution consisting of a group of individuals who make set contributions and withdrawals to and from a common fund. A ROSCA uses a common fund to which individuals contribute a set amount on a regular basis (usually monthly), while one member withdraws the funds at each meeting.

Although the Help-To-Invest scheme hibretOne is not quite the traditional ROSCA, many of the fundamentals around community, saving and using funding to impact lives are the same. We are aiming to give it a modern technological twist.

The global Rotating Savings & Credit Association (ROSCA) market is worth $790billion. Help-To-Invest we hope will allow us to tap into this levelling-up opportunity.

A rotating savings and credit association (ROSCA) is an informal financial institution consisting of a group of individuals who make set contributions and withdrawals to and from a common fund. A ROSCA uses a common fund to which individuals contribute a set amount on a regular basis (usually monthly), while one member withdraws the funds at each meeting.

Although the Help-To-Invest scheme hibretOne is not quite the traditional ROSCA, many of the fundamentals around community, saving and using funding to impact lives are the same. We are aiming to give it a modern technological twist.

In a ROSCA, members pool their money into a common fund, generally structured around monthly contributions, and a single member withdraws the money from it as a lump sum at the beginning of each cycle. This continues for as long as the group exists.

ROSCA is called ‘pardna’ in the Caribbean, ‘ajo’ in northern Nigeria, ‘Esusu’ and ‘Adashe’ in other areas. In India ROSCA’s have several names, ‘Kameti’ or ‘Chit’ being two of them. In Pakistan ‘visi’. ‘Cundinas’

In a ROSCA, members pool their money into a common fund, generally structured around monthly contributions, and a single member withdraws the money from it as a lump sum at the beginning of each cycle. This continues for as long as the group exists.ROSCA is called ‘pardna’ in the Caribbean, ‘ajo’ in northern Nigeria, ‘Esusu’ and ‘Adashe’ in other areas. In India

In a ROSCA, members pool their money into a common fund, generally structured around monthly contributions, and a single member withdraws the money from it as a lump sum at the beginning of each cycle. This continues for as long as the group exists.

ROSCA is called ‘pardna’ in the Caribbean, ‘ajo’ in northern Nigeria, ‘Esusu’ and ‘Adashe’ in other areas. In India ROSCA’s have several names, ‘Kameti’ or ‘Chit’ being two of them. In Pakistan ‘visi’. ‘Cundinas’ in Mexico, ‘hagbad’ in Somalia, ‘stokvels’ in South Africa and ‘Hui’ in China.

When Drew Currie, the founders’ parents came to the UK from the Caribbean, they could not get finance to purchase a home. The same was and still is true for many migrants to this country. So pooling together with friends in the community, allowed my parents to get the deposit for their first home. A home where my siblings and I were all born. Without a ROSCA many similar families would not have been started

ROSCAs are usually created in areas where access to formal financial institutions, such as banks, is limited. Members may share familial, ethnic, or geographical ties, and the structure of payments and withdrawals will vary according to the needs of the group. Recipients of funds may be chosen based on financial need, social standing, monetary bids, or random assignment.

By hibretOne being the organiser of the ROSCA we hope to bridge traditional familial, ethnic and geographical boundaries.

In a ROSCA, members pool their money into a common fund, generally structured around monthly contributions, and a single member withdraws the money from it as a lump sum at the beginning of each cycle. This continues for as long as the group exists.

ROSCA is called ‘pardna’ in the Caribbean, ‘ajo’ in northern Nigeria, ‘Esusu’ and ‘Adashe’ in other areas. In India ROSCA’s have several names, ‘Kameti’ or ‘Chit’ being two of them. In Pakistan ‘visi’. ‘Cundinas’ in Mexico, ‘hagbad’ in Somalia, ‘stokvels’ in South Africa and ‘Hui’ in China.

When Drew Currie, the founders’ parents came to the UK from the Caribbean, they could not get finance to purchase a home. The same was and still is true for many migrants to this country. So pooling together with friends in the community, allowed my parents to get the deposit for their first home. A home where my siblings and I were all born. Without a ROSCA many similar families would not have been started

ROSCAs are usually created in areas where access to formal financial institutions, such as banks, is limited. Members may share familial, ethnic, or geographical ties, and the structure of payments and withdrawals will vary according to the needs of the group. Recipients of funds may be chosen based on financial need, social standing, monetary bids, or random assignment.

By hibretOne being the organiser of the ROSCA we hope to bridge traditional familial, ethnic and geographical boundaries.

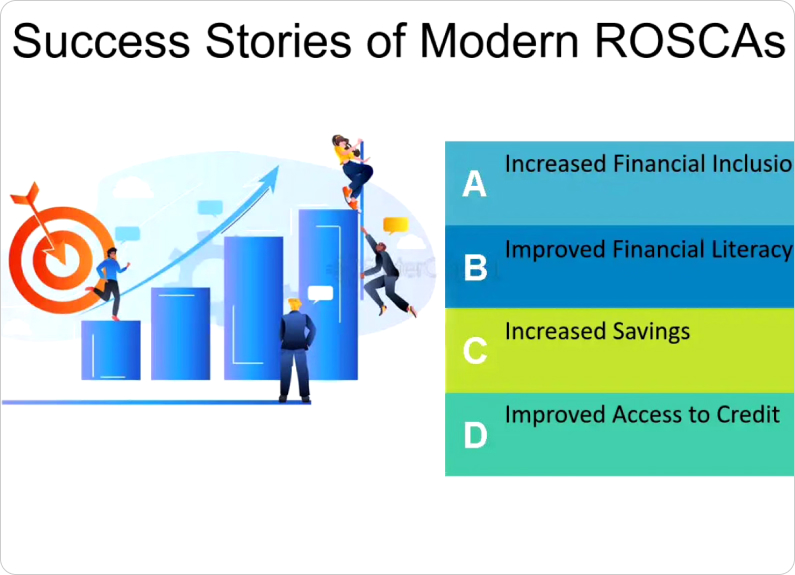

The principal advantages of ROSCAs are two-fold. First, they encourage personal savings, particularly among people without a lot of disposable income. Second, they provide a significant lump sum of money to individuals who might not be able to accumulate one otherwise. That individual might, for example in our case, use the lump sum to invest in a community business, social enterprise and high-profit potential enterprise.

Beyond providing funding to individuals who might not have access to a conventional banking system, ROSCAs have the

The principal advantages of ROSCAs are two-fold. First, they encourage personal savings, particularly among people without a lot of disposable income. Second, they provide a significant lump sum of money to individuals who might not be able to accumulate one otherwise. That individual might, for example in our case, use the lump sum to invest in a community business, social enterprise and high-profit potential enterprise.

Beyond providing funding

The principal advantages of ROSCAs are two-fold. First, they encourage personal savings, particularly among people without a lot of disposable income. Second, they provide a significant lump sum of money to individuals who might not be able to accumulate one otherwise. That individual might, for example in our case, use the lump sum to invest in a community business, social enterprise and high-profit potential enterprise.

Beyond providing funding to individuals who might not have access to a conventional banking system, ROSCAs have the added benefit of accountability. Knowing fellow participants or having an organisation to personally underwrite the investment can help build trust if members do not know each other that well. This includes making a commitment on how to use the funds. As well, money cannot be freely withdrawn, which can be a positive aspect for participants who would be inclined to spend it.

Money cannot be freely withdrawn, which can be a positive aspect for participants who would be inclined to spend it, but an issue if access to the capital is needed immediately.

ROSCAs have social benefits, as well. While the primary objective is usually to achieve the group's financial goals, ROSCA meetings can also provide opportunities for socialising and networking with people outside your traditional circles.

The principal advantages of ROSCAs are two-fold. First, they encourage personal savings, particularly among people without a lot of disposable income. Second, they provide a significant lump sum of money to individuals who might not be able to accumulate one otherwise. That individual might, for example in our case, use the lump sum to invest in a community business, social enterprise and high-profit potential enterprise.

Beyond providing funding to individuals who might not have access to a conventional banking system, ROSCAs have the added benefit of accountability. Knowing fellow participants or having an organisation to personally underwrite the investment can help build trust if members do not know each other that well. This includes making a commitment on how to use the funds. As well, money cannot be freely withdrawn, which can be a positive aspect for participants who would be inclined to spend it.

Money cannot be freely withdrawn, which can be a positive aspect for participants who would be inclined to spend it, but an issue if access to the capital is needed immediately.

ROSCAs have social benefits, as well. While the primary objective is usually to achieve the group's financial goals, ROSCA meetings can also provide opportunities for socialising and networking with people outside your traditional circles.

Many people are unaware of the issues Black Asian and Minority Ethnic have in accessing capital and the entrepreneurial ways these communities have had to overcome them. By educating everyone and sharing collaborative ROSCA’s hibretOne hopes to create community across cultures, religions, geographic linnes and ethnic origins.

Piloting this Help-To-Invest model in the W Midlands as one of the UK’s first super-diverse regions, makes complete sense. Working with the government, partners and community organisations we hope to launch when legislation allows.

Many people are unaware of the issues Black Asian and Minority Ethnic have in accessing capital and the entrepreneurial ways these communities have had to overcome them. By educating everyone and sharing collaborative ROSCA’s hibretOne hopes to create community across cultures, religions, geographic linnes and ethnic origins.

Piloting this Help-To-Invest model in the

Many people are unaware of the issues Black Asian and Minority Ethnic have in accessing capital and the entrepreneurial ways these communities have had to overcome them. By educating everyone and sharing collaborative ROSCA’s hibretOne hopes to create community across cultures, religions, geographic linnes and ethnic origins.

Piloting this Help-To-Invest model in the W Midlands as one of the UK’s first super-diverse regions, makes complete sense. Working with the government, partners and community organisations we hope to launch when legislation allows.

Many people are unaware of the issues Black Asian and Minority Ethnic have in accessing capital and the entrepreneurial ways these communities have had to overcome them. By educating everyone and sharing collaborative ROSCA’s hibretOne hopes to create community across cultures, religions, geographic linnes and ethnic origins.

Piloting this Help-To-Invest model in the W Midlands as one of the UK’s first super-diverse regions, makes complete sense. Working with the government, partners and community organisations we hope to launch when legislation allows.

The information or service is for informational purposes only and is not intended to be personal financial advice.

hibretOne is not an approved finance provider and until the investment products are launched encourages all interested parties to seek financial advice.

There's an inherent risk involved with financial decisions and the website owner will not be held liable for decisions others make.

The information or service is for informational purposes only and is not intended to be personal financial advice.

hibretOne is not an approved finance provider and until the investment products are launched encourages all interested parties to seek financial advice.

The information or service is for informational purposes only and is not intended to be personal financial advice.

hibretOne is not an approved finance provider and until the investment products are launched encourages all interested parties to seek financial advice.

There's an inherent risk involved with financial decisions and the website owner will not be held liable for decisions others make. Investments can go up as well as down.

Past performance is not a reliable indicator of future results. The value of investments and the income therefrom may go down as well as up and investors may not get back the original amount invested. You are not guaranteed to make money from your investments and you may lose money.

The FCA defines investment-based crowdfunding as a platform where “consumers may invest directly or indirectly in new or established business by buying investments such as shares or debt securities.

The rules include the following: Platforms may work only with clients who meet specific criteria:

- High net worth or sophisticated investors such as VCs and high-net-worth individuals.

- Clients who take regulated advice.

- Clients who can confirm that they will invest less than 10% of their net assets in a specific security.

The information or service is for informational purposes only and is not intended to be personal financial advice.

hibretOne is not an approved finance provider and until the investment products are launched encourages all interested parties to seek financial advice.

There's an inherent risk involved with financial decisions and the website owner will not be held liable for decisions others make. Investments can go up as well as down.

Past performance is not a reliable indicator of future results. The value of investments and the income therefrom may go down as well as up and investors may not get back the original amount invested. You are not guaranteed to make money from your investments and you may lose money.

The FCA defines investment-based crowdfunding as a platform where “consumers may invest directly or indirectly in new or established business by buying investments such as shares or debt securities.

The rules include the following: Platforms may work only with clients who meet specific criteria:

- High net worth or sophisticated investors such as VCs and high-net-worth individuals.

- Clients who take regulated advice.

- Clients who can confirm that they will invest less than 10% of their net assets in a specific security.

Funding, research and opportunities delivered directly to your inbox